CIBIL Score India: What It Is, Why It Matters More Than You Think, and How to Improve It Fast in 2026

Your CIBIL score is a three-digit number between 300 and 900. It sits quietly in a database, updated every fortnight now under new RBI rules, and it affects things in your life that have nothing to do with borrowing money. Most salaried Indians either don’t know their CIBIL score or only think about it when they’re filling a home loan application. Both are mistakes.

A few months ago, a colleague applied for a home loan. He’d saved the down payment over three years, found a flat he liked, ran the EMI numbers, and walked into his bank feeling prepared. The loan officer ran a check and came back with a rate that was 1.25% higher than what his friend had got from the same bank a year earlier.

Same bank. Same loan amount. Same neighbourhood. Nearly ₹10 lakh more in total interest over 20 years. The only difference was their CIBIL scores.

That one number — a score most people don’t even know how to check — had just cost him ten lakhs.

This article covers everything about your CIBIL score: what it is, how it’s calculated, what the 2026 RBI rule changes mean for you, and exactly what to do to improve it as fast as legally possible.

What this guide covers

What is a CIBIL score and who calculates it?

CIBIL stands for Credit Information Bureau India Limited. The organisation is now officially called TransUnion CIBIL and is one of four RBI-licensed credit bureaus in India — the others being Equifax, Experian, and CRIF High Mark. When people say ‘CIBIL score’ in India, they almost always mean the TransUnion CIBIL score, though all four bureaus produce credit scores.

Every time you take a loan, use a credit card, or miss a payment, your lender reports this activity to the credit bureaus. The bureaus compile this data into a credit report and distil it into a single score — your CIBIL score.

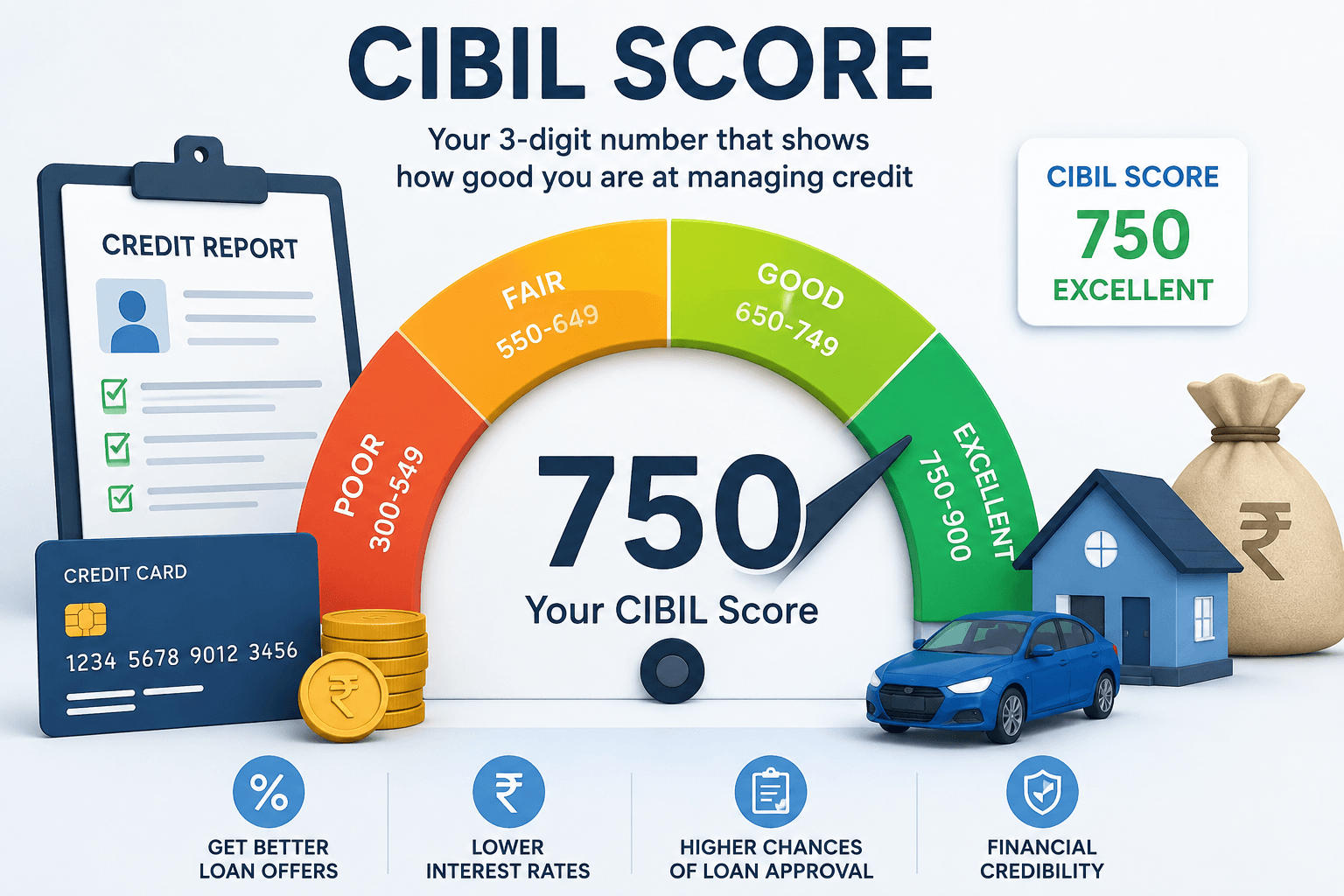

The score ranges from 300 to 900. The closer to 900, the better. Here’s what each range means in practice:

| CIBIL Score range | Category | What lenders think |

| 800 – 900 | Excellent | Best rates, instant approval, strong negotiating power |

| 750 – 799 | Good | Near-best rates, standard processing, most loans approved |

| 700 – 749 | Fair | Moderate rates, may need extra documentation |

| 650 – 699 | Below average | Higher rates, stricter loan-to-value limits, more scrutiny |

| 600 – 649 | Poor | Very high rates, limited lender options |

| 300 – 599 | Very poor | Most mainstream banks will reject outright |

The widely cited benchmark in India is 750. A CIBIL score of 750 and above is considered the minimum to access competitive home loan rates from major banks. A score of 800 or above puts you in a position to negotiate further.

How your CIBIL score is calculated

TransUnion CIBIL uses a weighted model based on five factors. Knowing the weights helps you prioritise what to fix first.

| Factor | Weight | What it means |

| Payment history | ~30% | Have you paid EMIs and credit card bills on time? |

| Credit utilisation | ~25% | What percentage of your credit card limit are you using? |

| Credit age / history length | ~25% | How long have you been using credit? |

| Credit mix | ~10% | Do you have both secured (home/car loan) and unsecured (credit card/personal loan) credit? |

| Recent enquiries / new credit | ~10% | How many times have lenders pulled your credit report recently? |

The most important takeaway: payment history and credit utilisation together make up more than half your score. Everything else is secondary. If you pay on time and keep your credit card usage low, you are already doing the two things that matter most.

The 2026 RBI rule change that speeds up CIBIL score improvement

This is the most significant update to how credit scores work in India in recent years, and most people don’t know about it.

Before January 2025, lenders were required to report your credit data to bureaus only once a month. This meant a payment you made on the 5th might not reflect in your CIBIL score until 35 to 45 days later. If you were trying to improve your score before applying for a loan, the slow reporting made it frustrating.

From January 2026, the RBI has mandated fortnightly reporting for all scheduled commercial banks and major NBFCs. Your credit data is now updated every 15 days. Several large lenders including SBI and HDFC are already reporting weekly voluntarily — meaning positive actions at those lenders can show in your CIBIL score within 7 to 15 days.

What this means practically:

- If you reduce your credit card utilisation today, it reflects in your score within one to two reporting cycles — not 30 to 45 days as before.

- If you dispute an error in your credit report, bureaus must now resolve it within 30 days and update the corrected data within 5 days of receiving confirmation from the lender.

- Missed payments also get flagged faster — within 15 days instead of up to 45 days previously. This cuts both ways.

One important clarification from the research: there is no “15-3 rule” for Indian CIBIL scores. That phrase appears in YouTube videos and informal articles but has no basis in RBI regulations. It comes from American FICO advice and does not apply to India. Ignore it.

What your CIBIL score actually affects in 2026

Most people associate the CIBIL score only with loan approvals. The reality is broader.

Home loan interest rate: This is the biggest financial impact. On a ₹50 lakh home loan over 20 years, the difference in interest rates between a CIBIL score of 800+ and one below 700 translates to ₹7 to ₹10 lakh in extra interest paid over the full tenure. That’s real money.

Here’s what home loan rates look like across score ranges in 2026 (indicative, based on publicly available bank rate structures):

| CIBIL Score | Indicative home loan rate | EMI on ₹50L / 20 yrs |

| 800+ | 8.25 – 8.50% | ₹43,391 – ₹43,391 approx |

| 750 – 799 | 8.50 – 8.75% | ₹43,391 – ₹44,373 approx |

| 700 – 749 | 8.75 – 9.25% | ₹44,373 – ₹46,607 approx |

| 650 – 699 | 9.25 – 10.00% | ₹46,607 – ₹48,251 approx |

| Below 650 | 10% or higher / rejection | Significantly higher or no loan |

Personal loan and credit card rates: Just like home loans, your CIBIL score determines the interest rate on personal loans. The difference between a 12% personal loan and an 18% one over a ₹5 lakh three-year loan is roughly ₹50,000 in extra interest. The same credit need, significantly different cost.

Credit card approval and limit: Banks check your CIBIL score before approving a credit card application and before enhancing your credit limit. A low score either gets the application rejected or results in a very low initial limit.

Employment in BFSI sector: Many banking, finance, insurance, and fintech employers now check credit scores as part of background verification for roles that handle money or client accounts. A poor CIBIL score can affect job prospects in this sector.

Rental agreements: Some landlords in metro cities — particularly for premium properties or co-living setups — now ask for a credit report before signing the agreement. Not universal, but increasingly common.

How to check your CIBIL score for free

You are entitled to one free credit report per year from each credit bureau under RBI mandate. Here’s how:

- Go to cibil.com and click ‘Get Free CIBIL Score & Report.’

- Register or log in with your PAN, date of birth, and mobile number.

- Verify via OTP.

- Your score and full report are displayed immediately.

Checking your own score is called a ‘soft inquiry’ and does not affect your CIBIL score at all. Only when a lender checks your score as part of a loan application does it create a ‘hard inquiry’ that slightly affects your score. Check your own score as often as you want — there’s no downside.

Several platforms also offer free CIBIL score checks — Paisabazaar, BankBazaar, OneScore, and CreditMantri among them. These are free and do not affect your score.

How to improve your CIBIL score fast — the ranked actions

There is no legal way to improve your CIBIL score overnight. Anyone promising that is either lying or describing something that will hurt your score later. But with the right actions, improvement within 60 to 90 days is genuinely achievable for most people.

Here are the actions ranked by speed of impact:

Action 1 — Dispute errors in your report (fastest, 30 days): Download your full credit report and read every line. Look for loans you didn’t take, payments marked late when you paid on time, accounts that show ‘active’ when you’ve closed them, or duplicate entries. These errors are more common than most people realise and can drag your score down significantly. Under the 2026 RBI framework, lenders must resolve disputes within 30 days. A corrected false default can cause a score jump of 30 to 100 points. Dispute directly on cibil.com under ‘Raise a Dispute.’

Action 2 — Reduce credit card utilisation below 30% (fast, 15 to 30 days with new reporting): If your credit card limit is ₹1,00,000 and you consistently use ₹70,000 of it, your utilisation is 70%. That’s treated as high-risk by scoring models. Bring it below 30% — ideally below 20% — as quickly as possible. Pay down the outstanding balance. With fortnightly RBI reporting in 2026, this improvement now reflects in your score within 15 to 30 days at many banks.

Action 3 — Pay every EMI and credit card bill in full and on time (ongoing, reflects within 15 days): Payment history is 30% of your score. Even one missed payment can drop your score by 50 to 100 points. Set up auto-pay for the full outstanding amount on every credit card, not just the minimum due. A minimum payment avoids the late fee but does not protect your CIBIL score — the outstanding balance still accrues interest and the reporting marks the account as ‘partially paid.’

Action 4 — Don’t apply for multiple loans or credit cards simultaneously (immediate): Every time a lender checks your CIBIL score as part of a loan application, it creates a hard inquiry. Multiple hard inquiries in a short period signal financial distress to scoring models and drop your score. If you need a loan, apply to one lender at a time. Compare rates on aggregator platforms without applying first — those are soft inquiries.

Action 5 — Keep old credit cards open (ongoing): The age of your credit history contributes to your score. Closing your oldest credit card — even if you don’t use it — reduces your average credit age and can drop your score. If there’s no annual fee, keep it active with one small transaction every 6 months.

Action 6 — Clear overdue or settled accounts (medium-term, 3 to 6 months): If you have any account marked ‘settled’ (meaning you paid less than the full amount as a one-time settlement) or ‘written off,’ it stays on your credit report for seven years and significantly damages your score. Contact the lender, pay the remaining amount in full, and request an NOC and a status update to ‘Closed’ on the bureau. This process takes time but removes one of the most damaging entries on a credit report.

Realistic timelines for CIBIL score improvement

| Starting score | Target score | Realistic timeline | Primary actions |

| 750+ | 800+ | 3 – 6 months | Reduce utilisation, no new enquiries, consistent payments |

| 700 – 749 | 750+ | 3 – 6 months | On-time payments, reduce utilisation, dispute errors |

| 650 – 699 | 720+ | 4 – 8 months | Dispute errors, clear overdue, reduce utilisation |

| 600 – 649 | 700+ | 6 – 12 months | All of the above plus clearing settled/written-off accounts |

| Below 600 (settlement/written off) | 650+ | 12 – 18 months | Full repayment of settled accounts, consistent new payments |

The most important insight: if you have a loan settlement or written-off account on your report, there is no shortcut. The seven-year clock only resets when you clear the account and get it marked as ‘Closed.’ For everything else, consistent behaviour over 4 to 6 months gets most people where they need to be.

What not to do — CIBIL score myths that will hurt you

- Do not close all your credit cards thinking zero credit = good credit. Zero credit history often scores lower than moderate responsible usage.

- Do not take a personal loan ‘just to build credit.’ The interest cost is real. Build credit through a credit card used responsibly instead.

- Do not use a credit repair company that promises to ‘clean’ your CIBIL report. These companies often charge large fees to do things you can do yourself for free — raise disputes on cibil.com. There is no legal way to remove accurate negative information.

- Do not apply for multiple credit cards in a short period to ‘increase available credit.’ Each application is a hard inquiry. Multiple hard inquiries drop your score.

- Do not ignore your credit report because you haven’t borrowed in years. Errors can appear even on dormant files.

Your CIBIL score action plan for this week

You don’t need a month to start. Here’s what to do in the next seven days:

- Day 1: Download your free CIBIL report from cibil.com using your PAN.

- Day 2: Read every entry. Mark anything that looks incorrect, unfamiliar, or shows a wrong status.

- Day 3: Log in and raise a dispute for every incorrect entry.

- Day 4: Check your credit card outstanding balance. Calculate your utilisation percentage (balance / limit x 100). If it’s above 30%, make a payment to bring it down.

- Day 5: Set up auto-pay on every credit card for the full outstanding amount, not minimum due.

- Day 6: Check if you have any overdue or settled accounts. If yes, call the lender and ask for the full repayment amount and process.

- Day 7: Delete any loan comparison or credit card comparison app where you’ve given permission for hard enquiries without intending to apply.

My colleague who got the higher home loan rate? He spent six months after that fixing his CIBIL score — paid down his credit cards, disputed one incorrect entry, and waited out the reporting cycles. He refinanced the loan at a lower rate once his score crossed 780. The process was slow and annoying, but it worked. The interest saving over the remaining tenure of his loan will be significant.

Your CIBIL score is not destiny. It’s a number that reflects your past behaviour, and past behaviour can be changed. The people who understand this — and act on it before they need a loan, not after — are the ones who get the best rates, the fastest approvals, and ultimately pay the least for the money they borrow.

Start with the report. Everything else follows from that.

Related reading on The Salary Investor:

• Credit Card vs Personal Loan India 2026: Which Is Actually Cheaper?

• Emergency Fund India 2026: How Much Is Enough and Where to Keep It

• How Much Term Insurance Do I Actually Need? A Salaried Indian’s Honest Guide

• What Happens to Your Money If You Never Invest It — The Real Cost of Doing Nothing

Disclaimer: CIBIL score ranges, home loan rate structures, and improvement timelines mentioned in this article are based on publicly available data from lenders, credit bureaus, and verified sources as of 2026. Actual home loan rates vary by bank, loan amount, loan-to-value ratio, income profile, and individual lender policies at the time of application. RBI fortnightly reporting mandate is confirmed from Wishfin (March 2026) and ProfitNifty (April 2026). Dispute resolution timelines are per RBI guidelines as reported by these sources. This article is for general educational purposes only and does not constitute financial or legal advice. Please verify current rates with your lender and consult a certified financial planner for decisions specific to your situation.

Sources: RBI fortnightly reporting from January 2026, dispute resolution 30 days (Wishfin, March 10, 2026) · Fortnightly reporting — positive actions reflect in score within 15 days; no 15-3 rule in India (ProfitNifty, April 11, 2026) · 600 to 750 in 4–6 months; dispute can improve score 30–100 points within 45 days; CIBIL score affects BFSI employment (Beincareer, March 17, 2026) · Home loan rates by CIBIL score — 800+ 8.25–8.50%, 650–699 9.25–10%; 1% difference = ₹7–8L extra on ₹50L loan (Money Matrix Hub, February 5, 2026) · 800+ CIBIL score saves over ₹3.5 lakh vs below 700 on ₹50L home loan (GoCredit, April 12, 2026) · Payment history 30%, credit utilisation 25% of CIBIL score; 750+ ideal for home loan (CreditHelpIndia, November 2025)

He figured out most of what he knows about personal finance not from courses or advisors, but from years of reading, making mistakes, and fixing them. The Salary Investor is his attempt to save other salaried Indians the same time and money.

He is not a CA or a SEBI-registered advisor. He writes as a fellow salaried person who has been in the trenches — navigating EPF, ITR, 80C, salary slips, and market volatility.

- Flexi Pay Allowances in India: What You Can Actually Claim and What You Can’t (2026) - July 20, 2026

- How a Salary Increment Affects Your Tax Bracket — and What to Do in March Before the New Package Kicks In - July 19, 2026

- NSC vs SCSS vs Post Office FD: Which Government Scheme Wins for Conservative Investors in 2026? - July 18, 2026