The 50-30-20 Budget Rule: Does It Actually Work on an Indian Salary?

My colleague Ankit earns ₹65,000 a month. Decent salary. No bad habits. Doesn’t gamble, doesn’t party every weekend. But by the 22nd of every month, his account shows ₹3,400. He came to me genuinely baffled. That’s when I introduced him to the 50-30-20 rule India budgeting framework — and more importantly, showed him why his numbers were breaking it without him even realising.

The 50-30-20 rule has been around for decades. It was popularised by US Senator Elizabeth Warren in her 2005 book All Your Worth. It’s taught in every personal finance 101 class. And almost every article about it makes it sound simple and foolproof.

It is simple. Foolproof is where things get complicated — especially on an Indian salary in 2026, where rent can eat half your take-home before you’ve bought a single grocery item.

This article gives you the honest version: what the rule actually says, what it means for real Indian salaries, where it breaks down, and how to make it work for you even when the numbers don’t fit neatly into three buckets.

What this article covers

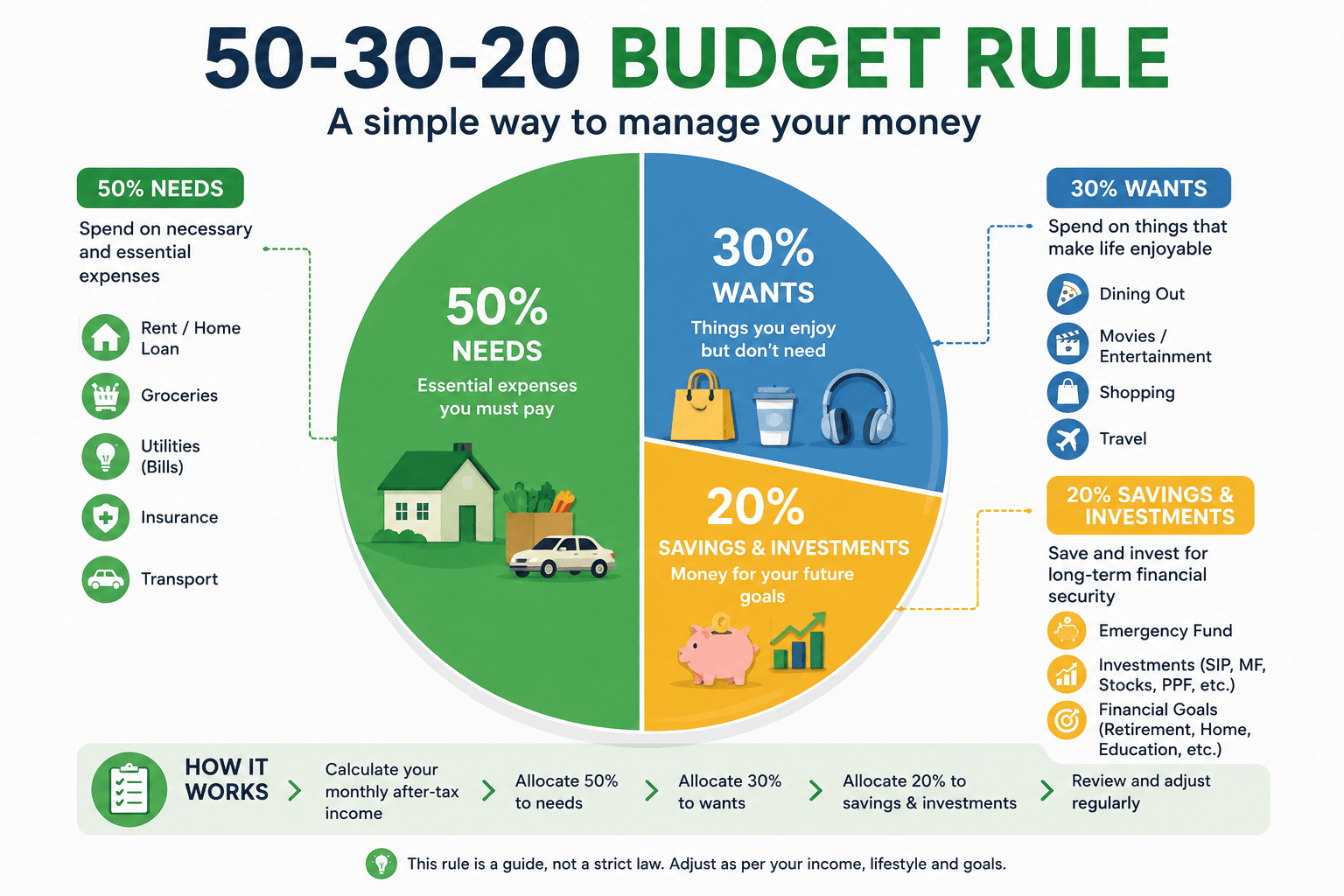

What the 50-30-20 budget rule in India actually says

The rule divides your monthly income into three buckets. That’s the entire concept. Everything else is just implementation.

50% goes to Needs. 30% goes to Wants. 20% goes to Savings and investments.

Before anything else — and this matters enormously in India — the 50-30-20 rule works on your take-home salary, not your CTC.

This distinction trips up a huge number of people. If your CTC is ₹12 lakh per annum, your monthly CTC is ₹1 lakh. But your actual take-home after EPF deduction, professional tax, and TDS is likely ₹74,000 to ₹78,000. Apply the rule to ₹1 lakh and your buckets are wrong from the start.

Always start with the number that hits your bank account. Check your latest salary slip or bank statement. That’s your base.

The three buckets — what actually goes where in India

50% — Needs (the non-negotiables): These are expenses you cannot cut without disrupting your basic functioning. In the Indian context, this includes rent or home loan EMI, groceries and household supplies, utilities (electricity, water, gas, internet, mobile recharge), school or college fees, insurance premiums (health and term), medicines and regular medical expenses, maid or cook salary if essential to your household running, and essential transport (fuel or monthly pass).

What does NOT go here: dining out, OTT subscriptions, gym membership, shopping, weekend plans. Those are wants, even if they feel like necessities.

30% — Wants (the things that make life enjoyable): This bucket covers everything you spend on by choice. Restaurant meals, movies, Swiggy and Zomato orders, holidays, new clothes beyond the basics, gadgets, streaming services, weekend activities. The rule doesn’t ask you to eliminate these — it just puts a ceiling on them.

The 30% wants bucket is the most debated part of this rule in the Indian context, and for good reason. In a metro city with high rent, getting 50% to stick to needs often means the wants bucket shrinks naturally. That’s fine — the rule is a guideline, not a law.

20% — Savings and investments: Everything that goes toward building your future: SIP contributions, PPF deposits, NPS contributions, EPF voluntary top-up, emergency fund building, loan prepayments, and any other goal-based saving. Your employer’s EPF deduction counts here too since it’s your money being saved, even if you don’t see it in your account.

The RBI data that changes how you think about the 50-30-20 budget rule

Here’s a number that should stop you mid-scroll.

The 50-30-20 rule recommends saving 20% of your income. According to the Reserve Bank of India’s Annual Report 2024-25, India’s net household financial savings stood at just 5.1% of gross national disposable income in FY 2023-24. Up from 4.9% the previous year, but still a fraction of what the rule recommends.

Even on an optimistic trajectory — SBI Research projects net financial savings may touch 6.5% of GNDI in FY 2024-25 — the average Indian household is saving roughly a third of what the rule recommends. Not because Indians are reckless. But because the cost of living, especially in cities, has grown faster than income.

Gross financial savings (before subtracting liabilities) are 11.2% of GNDI. Financial liabilities — home loans, personal loans, credit card debt — account for 6.1%. The net result is 5.1%.

This doesn’t mean the 50-30-20 rule is wrong. It means most people aren’t following it — and the gap between the recommended 20% and the actual 5.1% is exactly the space where financial stress lives.

Does the 50-30-20 budget rule actually work in Indian metro cities?

Let’s run the numbers honestly for a common scenario.

Priya earns ₹60,000 take-home per month. She lives in a 1BHK in Pune’s Baner area. Here’s what her month looks like:

| Expense | Monthly amount | Bucket | % of income |

| Rent | ₹20,000 | Need | 33.3% |

| Groceries + household | ₹7,000 | Need | 11.7% |

| Utilities + mobile + internet | ₹2,500 | Need | 4.2% |

| Health insurance premium | ₹1,500 | Need | 2.5% |

| Total Needs | ₹31,000 | — | 51.7% |

| Dining out + Swiggy | ₹5,000 | Want | 8.3% |

| Entertainment + OTT | ₹1,500 | Want | 2.5% |

| Shopping + personal care | ₹3,000 | Want | 5% |

| Weekend plans | ₹2,000 | Want | 3.3% |

| Total Wants | ₹11,500 | — | 19.2% |

| SIP | ₹5,000 | Savings | 8.3% |

| Emergency fund building | ₹3,000 | Savings | 5% |

| EPF (employer deducts) | ₹2,880 | Savings | 4.8% |

| Total Savings | ₹10,880 | — | 18.1% |

| Remaining (buffer) | ₹6,620 | — | 11% |

Priya’s needs are at 51.7% — just barely over the 50% ceiling. Her wants are at 19.2% — well under the 30% limit. Her savings are at 18.1% — close to the 20% target when you include EPF. She’s actually doing reasonably well.

But notice what it took: rent at ₹20,000 (a modest 1BHK in Pune’s decent area, not a premium flat), bare-minimum wants spending, and a disciplined SIP. For someone paying ₹25,000 to ₹30,000 in rent in Mumbai or Bengaluru, the 50% needs limit breaks almost immediately.

When the 50-30-20 budget rule breaks in India — and what to do

The rule struggles with four common Indian situations. Here’s how to adapt without abandoning the framework:

Situation 1 — High rent city (Mumbai, Bengaluru, Delhi): Rent alone eats 40%+ of take-home in these cities for anyone renting alone. The fix: accept a temporary 60-20-20 split (60% needs, 20% wants, 20% savings). The critical thing is that the savings bucket stays at 20% even when needs push higher. Cut wants first, not savings.

Situation 2 — Large home loan EMI: If your EMI + rent equivalent exceeds 40% of take-home, the 50% needs bucket fills up fast. Don’t try to artificially hit 50% by misclassifying EMI as savings. Home loan EMI is a need. Acknowledge it, accept a modified split, and focus on not letting wants creep up to compensate.

Situation 3 — Supporting parents or family: This is deeply Indian and the rule doesn’t account for it explicitly. Monthly transfers to parents, family medical costs, or sibling’s education costs should go in the Needs bucket — not Wants. They are obligations, not discretionary. This may push your needs above 50%, which is why a 55-25-20 or 60-20-20 split is more realistic for single-income households with dependents.

Situation 4 — Early career, low salary: On ₹25,000 to ₹35,000 take-home, hitting 20% savings while paying rent in a metro city is genuinely difficult. Don’t let perfect be the enemy of good. Save 10%. Get the habit. Increase it by 1% every six months. At ₹25,000 take-home, ₹2,500 in savings is still ₹30,000 in a year. The compound journey starts from anywhere.

The 20% savings bucket — how to split it

Most articles stop at “save 20%” without telling you what to do with that 20%. Here’s a practical split that works for most salaried Indians:

| Priority | Instrument | Suggested % of savings bucket | Why first |

| 1st | Emergency fund (liquid fund) | 25% of savings bucket (until 6 months built) | Protects everything else |

| 2nd | SIP — Nifty 50 index fund | 50% of savings bucket | Long-term wealth creation |

| 3rd | PPF / NPS | 15% of savings bucket | Tax saving + guaranteed growth |

| 4th | Discretionary goals | 10% of savings bucket | Down payment, travel fund, etc. |

In rupees, on a ₹60,000 take-home with 20% savings (₹12,000): ₹3,000 to emergency fund until you have 6 months built, ₹6,000 to SIP, ₹1,800 to PPF or NPS, and ₹1,200 for a specific goal. That’s a real plan, not just a percentage.

The five mistakes Indians make with the 50-30-20 budget rule

Mistake 1 — Applying the rule to CTC, not take-home: Covered above but worth repeating. Your 20% savings target on ₹1 lakh CTC is ₹20,000. Your 20% on ₹75,000 take-home is ₹15,000. That’s a ₹5,000 gap per month, which is ₹60,000 a year of miscalculation.

Mistake 2 — Counting EPF as savings without checking: Your EPF deduction is savings — but only your employee contribution (12% of basic). The employer’s contribution is part of CTC, not take-home. Don’t count money you never received as savings.

Mistake 3 — Skipping the emergency fund to invest more: Putting ₹12,000 straight into SIP when you have zero emergency fund is building a house without a foundation. One unexpected ₹30,000 expense and you break the SIP at a bad time.

Mistake 4 — Letting wants expand with every increment: This is the most insidious one. Salary goes from ₹60,000 to ₹72,000. Rent stays the same. Instead of increasing savings, the extra ₹12,000 goes to a nicer restaurant, a new phone, a bigger Swiggy budget. Wants expand to fill available space. The fix is to increase your SIP by the same day your increment hits.

Mistake 5 — Treating the rule as fixed instead of evolving: The 50-30-20 split that works at 27 while renting alone changes completely at 32 with a home loan and a child. Revisit your buckets every April after your increment letter arrives. Not obsessively — just once a year.

How to apply the 50-30-20 budget rule starting this week

This doesn’t require a spreadsheet or a budgeting app. Three steps, 20 minutes.

Step 1 — Find your actual take-home: Open your bank app. Look at the credit on the last salary day. That’s your number. Write it down.

Step 2 — List your fixed expenses (Needs): Write down every non-negotiable monthly cost: rent/EMI, groceries estimate, utilities, insurance, school fees, medicine, maid. Add them up. Divide by your take-home. If it’s under 50%, you’re in a good position. If it’s over, you know where the pressure is coming from.

Step 3 — Automate the savings bucket first: Before you touch a single rupee of your next salary, set up an auto-debit for your SIP 2 days after salary credit. Even if it’s just ₹3,000 to start. The money that leaves your account before you see it is the money that actually gets saved. Everything else — wants, lifestyle, food delivery — adjusts to whatever is left.

That’s the system. Simple, not easy. The discipline is in step 3.

Ankit — the colleague from the opening — tracked his spending for one month after our conversation. His Needs were at 53%. His Wants were at 41%. His savings were at 6%.

Nothing dramatic needed to change. He cut Swiggy by half. He stopped three unused subscriptions. He automated a ₹5,000 SIP on salary day. Three months later, his Wants were at 28%, his savings were at 18%, and his account on the 22nd showed ₹14,000 instead of ₹3,400.

The 50-30-20 rule doesn’t require perfection. It requires awareness. Most people in India have no idea how much they’re spending on wants versus needs until they sit down for 20 minutes and look. That awareness alone is worth more than any budgeting app.

Related reading on The Salary Investor:

• What Happens to Your Money If You Never Invest It — The Real Cost of Doing Nothing

• Emergency Fund India 2026: How Much Is Enough and Where to Keep It

• SIP vs PPF: Which One Should a Salaried Person Pick?

• How to Read Your Salary Slip — Every Component Explained in Plain English

• Old Tax Regime vs New Tax Regime: Which One Should You Pick in FY 2025-26?

Disclaimer: Net household financial savings figure of 5.1% of GNDI for FY 2023-24 and gross financial savings of 11.2% of GNDI are from RBI Annual Report 2024-25, released May 29, 2025, as reported by Business Standard (May 30, 2025). SBI Research projection of net financial savings touching 6.5% of GNDI in FY 2024-25 is from Business Standard (May 30, 2025). All salary and expense figures used in examples are illustrative. The 50-30-20 rule is a general budgeting framework and may not suit all income levels, cities, or family structures. This article is for general educational purposes only and does not constitute financial advice. Please consult a certified financial planner for advice specific to your situation.

Sources: RBI Annual Report 2024-25 — net household financial savings 5.1% of GNDI, gross financial savings 11.2% of GNDI in FY 2023-24 (Business Standard, May 30, 2025) · SBI Research — net financial savings projected at 6.5% of GNDI in FY 2024-25 (Business Standard, May 30, 2025) · 50-30-20 rule applies to take-home salary, not CTC — India context (Shriram Life, April 19, 2026) · 50-30-20 rule more relevant in 2026 due to rising inflation and lifestyle costs (CapitalSight, January 2026) · 50-30-20 rule — modified splits 60-20-20 for high-rent cities (Banking Unfold, August 2025) · India household savings RBI data — gross savings 30.3% of GNDI, financial liabilities 6.1% (IndiaGraphs, sourced from RBI Handbook of Statistics 2025)

He figured out most of what he knows about personal finance not from courses or advisors, but from years of reading, making mistakes, and fixing them. The Salary Investor is his attempt to save other salaried Indians the same time and money.

He is not a CA or a SEBI-registered advisor. He writes as a fellow salaried person who has been in the trenches — navigating EPF, ITR, 80C, salary slips, and market volatility.

- Flexi Pay Allowances in India: What You Can Actually Claim and What You Can’t (2026) - July 20, 2026

- How a Salary Increment Affects Your Tax Bracket — and What to Do in March Before the New Package Kicks In - July 19, 2026

- NSC vs SCSS vs Post Office FD: Which Government Scheme Wins for Conservative Investors in 2026? - July 18, 2026