How to Improve Your CIBIL Score — What Actually Works in 2026

Vikram works in Bengaluru, earns ₹85,000 a month, and hadn’t missed a single EMI or credit card payment in two years. When he applied for a home loan in early 2026, his bank offered him an interest rate 0.75% higher than what a colleague with a similar profile received. The difference? A CIBIL (Credit Information Bureau India Limited) score of 688 versus 762.

On a ₹50 lakh loan over 20 years, that 0.75% gap means roughly ₹6–8 lakh extra in total interest — based on home loan comparison data from Wishfin and mymudra.com (2026). That’s not rounding error. That’s a car. Or three years of a child’s school fees.

The frustrating part: Vikram’s score was fixable. He did it in five months without paying anyone a rupee. Here’s exactly what works — and what doesn’t.

What This Article Covers

What Is a CIBIL Score — and Why Does It Cost You Money

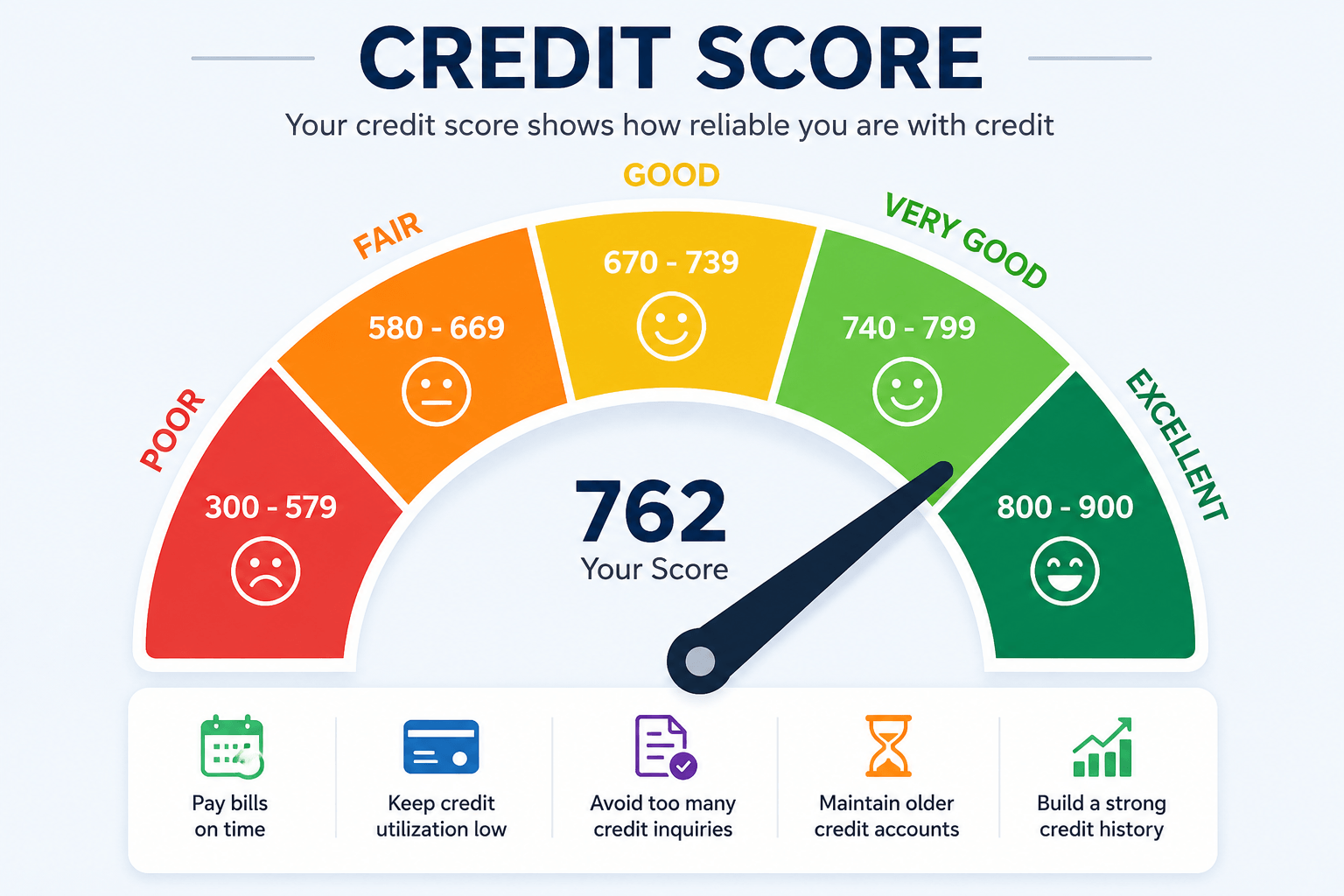

Your CIBIL score is a three-digit number issued by TransUnion CIBIL — a credit bureau licensed by the Reserve Bank of India (RBI) under the Credit Information Companies (Regulation) Act, 2005. The score ranges from 300 to 900. Higher is always better.

Most Indian banks want to see 750+ before offering their lowest interest rates. Below 700, expect higher rates, reduced loan eligibility, or outright rejections — especially on unsecured products like personal loans.

Here is what the score ranges signal in real terms (indicative; actual lender decisions vary):

| CIBIL Score Range | What It Signals | Typical Lender Response |

| 750–900 | Excellent credit behaviour | Best rates, fast approvals, premium credit cards |

| 700–749 | Good, some room to improve | Approvals likely, 0.25–0.50% rate premium |

| 650–699 | Moderate risk profile | Some approvals, 0.50–1% rate premium |

| 600–649 | Visible credit stress | Limited lenders, high rates, smaller limits |

| 300–599 | Serious credit problems | Mostly rejected by banks; some NBFCs may consider |

*Rate premium data is indicative, based on publicly available lender pricing structures (Wishfin, mymudra.com, 2026). Final rates depend on the lender’s own risk assessment.*

The score does not measure your income or your savings. It measures one thing: how reliably you’ve handled borrowed money, based on data that banks and NBFCs (Non-Banking Financial Companies) report to CIBIL every fortnight.

What Actually Determines Your CIBIL Score

TransUnion CIBIL does not publish its exact formula, but the broad factors and approximate weightings are consistently reported across industry sources:

Payment history — roughly 35% weight

The single biggest driver. Every EMI and credit card bill paid on time strengthens this. One missed payment can drop a healthy score by 50–80 points and stays on your record for years. This is not recoverable quickly — which is why preventing misses matters more than anything else.

Credit Utilisation Ratio (CUR) — roughly 30% weight

This is the percentage of your total credit card limit you are using at any point. If your card limit is ₹1 lakh and you are carrying a balance of ₹40,000, your CUR is 40%. Lenders see anything above 30% as a sign of credit dependency. For scores above 800, aim below 10%.

Length of credit history — roughly 15% weight

How long you have held credit. Older accounts carry more weight. This is why closing your oldest credit card — to simplify your wallet — can quietly hurt your score even if you have zero outstanding balance.

Credit mix — roughly 10% weight

A healthy spread of secured loans (home loan, car loan) alongside unsecured credit (credit cards) is viewed positively. But do not take loans purely to diversify your credit mix. It is a minor factor and the interest cost will not justify it.

New credit enquiries — roughly 10% weight

Every time you apply for a loan or credit card, the lender pulls your CIBIL report. This is a “hard enquiry” and causes a small, temporary score dip. Apply for five products in three months and it signals financial stress to any lender looking at your report.

What Changed in 2025 — Your Score Updates Faster Than Before

This is the most practically useful change for anyone improving their score right now.

Before 2025, banks reported credit data to bureaus once a month. If you paid off a large credit card balance on the 5th, that positive change might not appear in your score for 35–45 days.

From January 1, 2025, the RBI mandated that all lenders update credit bureau records every 15 days — on the 15th and the last working day of each month. This is confirmed in the RBI’s formal credit information reporting directions, reported by Business Standard (August 2024). The full updated Credit Information Companies (CICs) directions have been extended by RBI to take effect from July 1, 2026 (Business Standard, December 2025), but the fortnightly reporting requirement has been in force since January 2025.

What this means practically: Good credit behaviour now shows up in your score within two to three weeks, not five to six weeks. If you are working on improvement, you will see movement faster than at any earlier point.

One clear myth to dismiss: there is no “15-3 rule” for Indian CIBIL scores. That is an American FICO tip that gets misapplied to India constantly. Ignore any YouTube video or article mentioning a CIBIL “15-3 rule” — it has no basis in Indian credit reporting.

The 6-Step Action Plan: How to Go from 650 to 750+ in 3–6 Months

These steps are ranked by impact. Do them in this order.

Step 1: Pull your free CIBIL report and actually read it

TransUnion CIBIL gives you one free credit report per calendar year at cibil.com — a right granted by the RBI. As confirmed on CIBIL’s official website, if you’ve already used your 2026 free report, your next one is due January 1, 2027.

Beyond the annual free report, you can check your score anytime — for free and with zero impact to your score — on apps like CRED, Paytm, or BankBazaar. Checking your own score is a “soft enquiry.” It does not affect your score in any way.

When you open your full report, look for:

- Loans marked as “settled” instead of “closed”

- Accounts you do not recognise

- EMIs showing as overdue when you know you paid them

- Old loans or credit cards still showing as “active” after closure

Step 2: Fix errors immediately — they could be the main problem

Errors in CIBIL reports are more common than most people expect. If you find one, raise a dispute directly on the MyCIBIL portal at cibil.com. The process is digital, free, and straightforward. As per RBI guidelines confirmed on CIBIL’s official dispute page, disputes must be resolved within 30 days. If the deadline is missed, CIBIL and the lender are liable to pay ₹100 per day as compensation.

Fixing a genuine error can improve your score by 30–50 points within a single update cycle — faster than almost any other action.

Step 3: Pay every EMI and bill on time — without a single miss

This is the 35% factor. Set up auto-pay for the minimum due amount on every credit card so a forgotten payment never becomes a missed payment. Then manually pay the full outstanding balance on or before the due date each month.

If you have an old overdue amount you’ve been ignoring — a ₹2,000 overdue from a credit card three years ago, a forgotten mobile bill — pay it this week. Small unresolved overdues do disproportionate damage because they remain flagged “overdue” on your report indefinitely.

Step 4: Bring your Credit Utilisation Ratio below 30%

If you are regularly using more than 30% of your credit card limit, this is likely dragging your score down on every update cycle. Two ways to fix it:

Pay down the balance. If your limit is ₹1 lakh and you usually carry ₹50,000, bring it below ₹30,000.

Request a credit limit increase. If your income has grown since you first got the card, call your bank and ask. HDFC, ICICI, and Axis Bank all allow limit increase requests online through net banking or their app. If your limit goes from ₹1 lakh to ₹1.5 lakh and your spending stays the same, your CUR drops from 50% to 33% automatically — without spending less.

Do not close old credit cards unless there is an annual fee you genuinely cannot justify. Closing a card reduces your total available credit (pushing up your CUR) and removes credit history from your report — both negatives.

Step 5: Stop all new loan and credit card applications for 3–4 months

During a score recovery period, every new application is a small step backward. Give yourself a clean quarter of zero new enquiries.

If you are comparing home loan rates, use platforms like BankBazaar or Paisabazaar first — these do soft checks to give you rate estimates and do not trigger hard enquiries. Only submit an actual application to the lender you have finally chosen.

Step 6: Use a secured credit card if your score is below 600

If your score is in the poor range (below 600) and banks are rejecting applications, a secured credit card — issued against a fixed deposit (FD) — is the most reliable rebuilding tool available.

You keep ₹10,000–₹25,000 in an FD as security, and the bank gives you a card with a limit roughly equal to that amount. Use it for small monthly expenses — groceries, subscriptions, utility bills. Pay the full balance every month. After six to nine months of consistent use, your score will begin climbing from that base.

SBI Card Unnati requires a minimum FD of ₹25,000 and charges no annual fee for four years (source: profitnifty.in, April 2026). It is one of the better-known options for score rebuilding.

Mistakes That Are Quietly Pulling Your Score Down

These are patterns common among salaried professionals who think they are managing credit responsibly.

Paying only the minimum due on credit cards

This avoids a late-payment mark, but it keeps your CUR high — and CIBIL sees that high utilisation every fortnight when your lender updates the data. It also means you are paying 36–42% annual interest on the remaining balance. The minimum due is a trap, not a strategy.

Closing your oldest credit card

Feels like tidying up. But it removes credit history and reduces your total available credit, which pushes your utilisation ratio upward. Both hurt your score. Keep old, zero-fee cards active — even if you barely use them. A ₹500 grocery purchase every few months is enough to keep the account live.

Co-signing a loan for someone

When you co-sign a loan for a family member or friend, that loan appears on your credit report too. If they miss a payment, it hits your score — and you have no control over whether they pay on time. Think carefully before agreeing to be a co-applicant or guarantor on any loan.

Applying for multiple loans or cards at the same time

Each application triggers a hard enquiry. Five enquiries in a quarter sends a signal to lenders that you may be in financial trouble. Space out applications by at least 3–4 months.

Not checking your report for years

Errors accumulate silently. Closed accounts stay “active.” An address mismatch from a 2019 loan can cause issues in 2026. Your CIBIL report can contain errors that have nothing to do with your actual behaviour — and you will not know until a lender tells you your application has been rejected.

What to Do This Week

- Visit cibil.com and download your free annual report if you haven’t this year. Read every section — especially the Accounts section.

- Calculate your Credit Utilisation Ratio for each card right now. Add up your total limits; add up your total outstanding balances. If the ratio is above 30%, that is your immediate priority.

- Set up auto-pay on every active EMI and credit card for the minimum amount, today.

- If you find any error in your report, raise a dispute at cibil.com/consumer-dispute-resolution. Free, digital, resolved within 30 days under RBI rules.

- Pay every outstanding due — even old, forgotten ones. Small dues do outsized damage.

- Make no new loan or credit card applications for three months. Let the improvements show.

Most people who follow these steps will see 30–50 point improvements within two or three update cycles. If you are at 650 with a clean report except for high utilisation and a few missed payments, reaching 750+ in four to five months is realistic — and it will not cost you a rupee.

Related Reading on The Salary Investor

- Credit Card vs Personal Loan — Which Is Smarter for Your Situation?

- How to Read Your Salary Slip — CTC, TDS, and Every Deduction Explained

- Emergency Fund in India: How Much You Need and Where to Keep It

- Old vs New Tax Regime 2025–26: Which One Saves You More?

- How to File Your ITR Yourself — The Complete Guide for Salaried Indians

- EPF Mistakes Salaried Employees Make — And How to Avoid Them

Disclaimer: Data in this article is as of June 2026. CIBIL score ranges, interest rate premiums, and lender eligibility criteria are indicative and subject to change at any time. Loan approval outcomes are not guaranteed and vary by individual profile and lender policy. This article is for general financial education only. Please consult a SEBI (Securities and Exchange Board of India)-registered financial advisor or a qualified CA (Chartered Accountant) before making financial decisions.

Sources: Free CIBIL Score and Report — TransUnion CIBIL Official, 2026 · Consumer Dispute Resolution — TransUnion CIBIL Official, 2026 · RBI Shortens Frequency of Bank Reports to Credit Information Companies — Business Standard, August 2024 · RBI Defers Credit Information Reporting Norms to July 1, 2026 — Business Standard, December 2025 · CIBIL Score New Rules 2025 — Poonawalla Fincorp, September 2025 · Home Loan Interest Rate Based on CIBIL Score — MyMudra, 2026 · Home Loan Interest Rates Based on Different Credit Scores — Wishfin, 2026

He figured out most of what he knows about personal finance not from courses or advisors, but from years of reading, making mistakes, and fixing them. The Salary Investor is his attempt to save other salaried Indians the same time and money.

He is not a CA or a SEBI-registered advisor. He writes as a fellow salaried person who has been in the trenches — navigating EPF, ITR, 80C, salary slips, and market volatility.

- The Real Cost of EMI-Based Lifestyle: How Credit Card EMIs and Personal Loans Are Silently Destroying Wealth for Salaried Indians - July 24, 2026

- Reverse Mortgage in India: Can Your Parents Use Their Home to Fund Retirement? - July 23, 2026

- Top-Up vs Super Top-Up Health Insurance: The ₹15,000 Decision That Could Save You ₹5 Lakh - July 22, 2026