The Hidden Costs of Owning a Car That Nobody Talks About

A ₹10 lakh car doesn’t cost ₹10 lakh. The hidden costs of owning a car push the true 10-year bill to somewhere between ₹20 and ₹25 lakh — and that’s for a budget hatchback, driven modestly, with no major accidents. Most buyers never run this number. They look at the EMI, compare it to their salary, and sign the forms. The dealership is delighted.

Nobody lies to you when you buy a car. The costs are all real — fuel, insurance, servicing, parking. But they’re never shown together, on the same page, at the same time. That’s the problem. Individually, each cost feels manageable. Collectively, they change the math entirely.

If you’re planning to buy a car — or already own one — this breakdown is the conversation your dealer never had with you. Real rupee numbers, real costs, no glossing over.

What this article covers

The On-Road Price Trap: ₹10 Lakh Becomes ₹11.5 Lakh Before You’ve Driven Anywhere

The price advertised on every car brand’s website — and the number most people Google — is the ex-showroom price. This is the manufacturer’s price including GST. It does not include what you actually pay when you collect the car.

The on-road price — the real total you pay the day you take delivery — adds several mandatory charges on top:

- Road tax: A state government levy calculated on the ex-showroom price. Rates range from 2.5% to 20% depending on your state and the vehicle’s price slab. Maharashtra charges around 13% on cars up to ₹10 lakh. Delhi charges approximately 4–8% on similar vehicles. On a ₹10 lakh car, this adds ₹40,000 to ₹1.3 lakh. (Source: MoRTH/RTO state-wise rate data, 2026)

- Registration fee: A fixed ₹600 charged by the Regional Transport Office (RTO), plus ₹1,500 hypothecation charge if you’re financing the car.

- High Security Registration Plate (HSRP) and FASTag: ₹230–₹400 for the mandated number plate, plus ₹500–₹600 for FASTag. Both are now mandatory across India.

- Tax Collected at Source (TCS): 1% of the ex-showroom price, applicable on cars priced above ₹10 lakh.

- First-year insurance: Bundled into the on-road price at most dealers. For a ₹10 lakh car, comprehensive insurance for year one typically runs ₹18,000–₹25,000.

Illustrative example: Rohan buys a mid-range petrol hatchback (ex-showroom Delhi: ₹10 lakh) in June 2026. After road tax (approx. 4% in Delhi), registration, HSRP, FASTag, and first-year comprehensive insurance, his on-road price comes to roughly ₹11.35–₹11.50 lakh. He’s spent ₹1.25–₹1.40 lakh before turning the ignition.

And he hasn’t driven a single kilometre yet.

The Loan Interest Cost Nobody Calculates Till It’s Too Late

Most people taking a car loan focus on the monthly EMI. That’s the number that has to fit inside the salary. The total interest paid over the full tenure — that number stays invisible.

As of June 2026, car loan interest rates from major lenders range from 7.45% (Canara Bank) to 9.85% (SBI upper end) for new cars. HDFC Bank’s rates start from 8.15%; ICICI Bank from 8.35%. (Source: BankBazaar, June 2026; Zee Biz, May 2026.)

Here’s the math nobody shows you upfront:

Assume Rohan finances ₹9 lakh (90% of the on-road price) at 9% per annum over 5 years. His EMI works out to approximately ₹18,681 per month. Over 60 months, he pays back ₹11,20,860 in total. On a ₹9 lakh loan, that’s ₹2,20,860 in interest alone — money that goes to the bank and buys him nothing tangible.

Stretch that to 7 years (84 months, now offered by most banks) at the same rate, and total interest jumps to roughly ₹3,20,000.

One more thing dealers rarely mention: a larger down payment of 30–40% of the on-road price can save enough interest over 5 years to comfortably cover 2–3 years of fuel. It’s the single most powerful lever you have on day one.

Also worth checking: your CIBIL score before applying. A score above 750 can get you rates near the lower end of a bank’s range. A score below 680 can add 1.5–2 percentage points — that’s ₹50,000–₹80,000 extra in total interest on a ₹9 lakh loan.

Depreciation: The Biggest Hidden Cost of Owning a Car That Never Sends You a Bill

Depreciation is the cost of owning something that loses value while you use it. Your car is worth less the moment it leaves the showroom — and it keeps falling every year. Yet depreciation never shows up in your bank statement. That’s what makes it genuinely dangerous for financial planning.

The Insurance Regulatory and Development Authority of India (IRDAI) has defined standard depreciation slabs for insurance purposes, which also give a fair picture of how market value falls:

| Car Age | IRDAI Depreciation Rate | Value of a ₹10 Lakh Car |

| Up to 6 months | 5% | ₹9,50,000 |

| 6 months – 1 year | 15% | ₹8,50,000 |

| 1 – 2 years | 20% | ₹8,00,000 |

| 2 – 3 years | 30% | ₹7,00,000 |

| 3 – 4 years | 40% | ₹6,00,000 |

| 4 – 5 years | 50% | ₹5,00,000 |

Source: IRDAI standard motor insurance depreciation schedule (irdai.gov.in). Market resale value may differ based on brand, condition, and demand.

So Rohan’s ₹10 lakh car — which he financed at 9% over 5 years — is now worth roughly ₹5 lakh in the used-car market after 5 years. He paid ₹11.5 lakh on-road, plus ₹2.2 lakh in interest, plus all running costs. The car he can sell is worth ₹5 lakh. That gap is what 5 years of car ownership actually costs — and nobody puts it on a slide at the showroom.

One partial solution: when buying comprehensive insurance, consider a zero-depreciation add-on cover. This eliminates the depreciation deduction from claim payouts if the car is damaged. It adds ₹2,000–₹5,000 to your annual premium but can save significantly on a claim.

Fuel: The Monthly Drain You Actually Notice

Fuel is the most visible ongoing cost — and also the one most people underestimate because they calculate it for ‘average usage’, not real-world daily commuting with traffic, AC running, and weekend use.

As of June 26, 2026, petrol prices stand at ₹102.12 per litre in Delhi and ₹111.21 per litre in Mumbai, per live data from Goodreturns. Bangalore is at ₹111.68 per litre; Hyderabad at ₹115.69 per litre.

A typical salaried professional driving 1,000–1,200 km per month will spend:

- Petrol car at 15 km/l mileage, Delhi prices: 1,000 km ÷ 15 × ₹102.12 = ₹6,808 per month

- Petrol car at 15 km/l mileage, Mumbai prices: 1,000 km ÷ 15 × ₹111.21 = ₹7,414 per month

Scale this to a full year in Mumbai: ₹7,414 × 12 = ₹88,968 — nearly ₹89,000 a year, just in fuel. Over 5 years at today’s prices: ₹4.45 lakh, conservatively. Real-world spend will be higher given fuel price trends.

Weekends, road trips, airport runs, and picking up kids add up faster than a daily office commute does. Most people forget to count these when they estimate.

Car Insurance: The Cost That Rises Every Time You Claim

Car insurance is mandatory in India under the Motor Vehicles Act. A third-party policy alone covers only damage to others. Most financial advisors recommend comprehensive insurance, which covers your own vehicle too.

For a ₹10 lakh car, comprehensive insurance typically costs ₹12,000–₹25,000 per year depending on the Insured Declared Value (IDV), city, and chosen add-ons. (Source: AutoIndiaDaily, April 2026.) The IDV itself falls with IRDAI depreciation slabs every year — so your insurance cover reduces in value while you continue paying a premium.

What most people don’t factor in:

- A single claim wipes out your No-Claim Bonus (NCB), which can be worth a 20–50% discount on your premium after 5 claim-free years. One small dent claim can cost you ₹15,000–₹20,000 in lost bonus over the following 2–3 years.

- Add-ons like zero-depreciation, roadside assistance, engine protect, and return-to-invoice cover are useful — but each adds ₹3,000–₹8,000 to the annual premium. Choose based on your car’s age and value, not just whatever the dealer bundles.

- Dealers often mark up insurance significantly. You are legally entitled to buy from any IRDAI-approved insurer. Comparing on Policybazaar or Coverfox typically saves ₹3,000–₹8,000 versus the dealer’s bundled price.

For a detailed look at how claim settlement ratios differ across insurers, see the TSI guide on claim settlement ratios in India for 2026.

Annual Servicing and Maintenance: It Only Gets More Expensive With Time

Every car needs periodic servicing — oil changes, filter replacements, brake inspections, tyre rotation, wheel alignment. For a petrol hatchback, a standard authorised service centre visit every 10,000 km or annually runs:

- Maruti Suzuki models: ₹3,500–₹7,000 per service (lowest authorised service costs among popular brands in India)

- Hyundai, Tata, Honda models: ₹5,000–₹12,000 per service depending on model and variant

- SUVs and larger vehicles: ₹10,000–₹25,000 per service at authorised centres

These are scheduled service costs only. Unscheduled repairs — a puncture, early brake pad wear from city traffic, a sensor fault, a cracked windshield — are separate. A set of four replacement tyres for a hatchback costs ₹12,000–₹30,000 and needs to be done every 40,000–50,000 km.

The pattern: maintenance costs are low and predictable in the first 3 years (mostly scheduled services). From year 4 onwards, costs increase as wear items need replacement. The ₹3,000 monthly maintenance budget that worked in year 2 often becomes ₹6,000–₹8,000 in year 5.

Having a well-funded emergency fund matters here — repair bills don’t come with advance notice, and turning to a credit card or personal loan in a repair emergency is expensive.

Parking, Tolls, and the Costs That Quietly Disappear From Your Account

This is where the real underestimation happens, particularly for salaried professionals in metro cities.

Parking

Monthly paid parking at a housing society or commercial complex in Bangalore, Pune, or Mumbai: ₹500–₹2,500 per month. Daily parking at malls, hospitals, airports, or office complexes in Tier 1 metros: ₹50–₹150 per hour. (Source: Exicom EV charging & parking guide, 2026.)

A professional working in a central business district without a designated parking spot can easily spend ₹2,000–₹4,000 per month just on parking. Over a year, that’s ₹24,000–₹48,000 — a number few monthly budgets explicitly track.

Tolls

If your daily commute involves a highway or expressway — increasingly common in Gurugram, Pune, and Hyderabad — FASTag toll charges can add ₹500–₹3,000 per month depending on route. A ₹200 daily toll translates to ₹4,000–₹4,400 per month for someone commuting 20–22 working days.

Pollution certificate and miscellaneous

A Pollution Under Control (PUC) certificate costs ₹80–₹150 and needs renewal every 6 months to 1 year depending on vehicle age. Traffic challans — speeding, wrong-side violations, parking fines — run ₹500–₹2,000 per incident and are now enforced via cameras in most metros. Small cost per incident; quietly large over years.

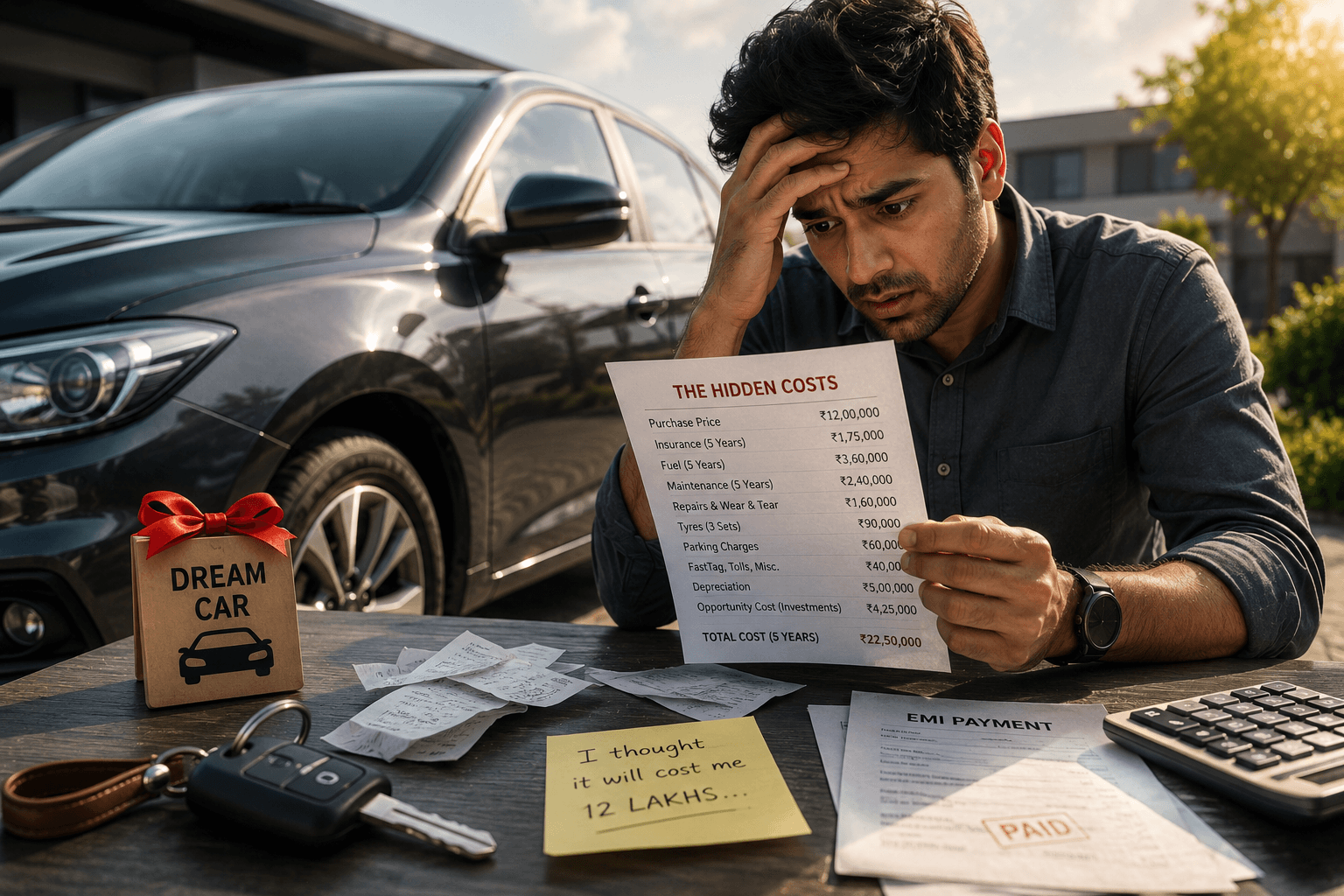

The Real Cost Table: What a ₹10 Lakh Car Actually Costs Over 5 Years

Here’s everything added up. These figures are illustrative estimates based on 2026 data. The car: a ₹10 lakh ex-showroom petrol hatchback, financed at 9% over 5 years, driven 1,000 km/month in Mumbai.

| Cost Head | Annual Estimate | 5-Year Total |

| On-road premium over ex-showroom (one-time) | ₹1,50,000 upfront | ₹1,50,000 |

| Loan interest (₹9L @ 9%, 5 yr) | ~₹44,000/yr avg | ~₹2,21,000 |

| Fuel (1,000 km/month, Mumbai, ₹111/litre) | ~₹89,000/yr | ~₹4,45,000 |

| Comprehensive insurance (incl. add-ons) | ₹18,000–₹22,000/yr | ~₹1,00,000 |

| Annual servicing and maintenance | ₹18,000–₹30,000/yr | ~₹1,20,000 |

| Tyres (1 full set, ~yr 4) | — | ~₹18,000 |

| Parking and tolls (Mumbai CBD estimate) | ₹36,000–₹60,000/yr | ~₹2,40,000 |

| Depreciation: market value lost over 5 years | Not a cash outflow | ~₹5,00,000 |

| Total cash spent (excl. depreciation) | ~₹12,94,000 | |

| Total economic cost (incl. depreciation loss) | ~₹17,94,000 |

Sources: Goodreturns (fuel, June 2026), IRDAI depreciation schedule, Zee Biz car loan data (May 2026), AutoIndiaDaily insurance estimates (April 2026). All figures are indicative.

That last row — roughly ₹18 lakh over 5 years on a ₹10 lakh car — is why the honest answer to ‘Can I afford this car?’ is never just the EMI. The EMI is the smallest piece of the number.

The Cost Nobody Mentions: What That Money Could Have Done Instead

This is the part financial advisors bring up and car salespeople definitely don’t.

The monthly running cost of that ₹10 lakh car in Mumbai — fuel, insurance (monthly equivalent), maintenance, parking — is roughly ₹12,000–₹15,000 per month, excluding the EMI itself.

₹10,000 invested every month via SIP in a Nifty 50 index fund from the same starting point would grow to approximately ₹8–₹8.5 lakh over 5 years at a 12% annualised return (illustrative, not guaranteed). That’s the rough scale of the opportunity cost.

This isn’t an argument against owning a car. For many salaried Indians — especially in cities with poor public transport, or families managing school runs and medical needs — a car isn’t a luxury. The point is to know the real number before signing, so the financial hit doesn’t come as a surprise 18 months in.

For a real look at how SIP compares to other decisions over time, see SIP vs Lump Sum: Which Strategy Actually Makes More Money. And if you’re weighing whether to put extra money into a loan or invest it, the analysis in Should You Prepay Your Home Loan or Invest? uses the same framework.

What to Do Right Now — Whether You’re Buying or Already Own

If you’re planning to buy

- Calculate the full on-road price using your state’s current RTO rate, not just the ex-showroom number. Use the Parivahan Sewa portal (parivahan.gov.in) or call your city’s RTO for the latest slabs.

- Add up your realistic 5-year total cost of ownership using the categories in this article before committing. The EMI alone is not the right affordability test.

- Buy your insurance separately — not from the dealer. Compare on Policybazaar (policybazaar.com) or Coverfox (coverfox.com). You can save ₹3,000–₹8,000 on year-one premium alone.

- Make the largest down payment you can manage without touching your emergency fund. Every extra rupee down reduces the interest over 5–7 years.

- Check your CIBIL score at CRIF Highmark (crifhighmark.com) or CIBIL (cibil.com) before applying for the loan. A better score means a lower rate — and on a ₹9 lakh loan, a 1% rate difference saves roughly ₹27,000 over 5 years.

If you already own a car

- Track your actual total monthly car cost this month — fuel, insurance equivalent, maintenance, parking, tolls. Add it all up. Most people are surprised by what they find.

- Review your insurance policy before the next renewal. Compare it against current market rates on aggregators. Check whether a zero-depreciation add-on is still worth it given your car’s current age and IDV.

- Set up a dedicated car maintenance sinking fund — put ₹2,000–₹3,000 there every month so unscheduled repairs don’t hit your emergency fund or credit card.

- If your car is over 5 years old, budget explicitly for rising maintenance costs. The ₹3,500 service that worked in year 2 is not the number you’ll see in year 6.

- If total car costs (EMI + all running expenses) exceed 15–20% of your take-home salary, something in the equation needs adjustment — the car, the loan tenure, or the commute pattern.

Related Reading on The Salary Investor

- Emergency Fund India 2026: How Much Is Enough and Where to Keep It

- CIBIL Score India: What It Is and How to Improve It Fast in 2026

- Claim Settlement Ratio: Which Insurers Actually Pay Up in 2026

- Credit Card vs Personal Loan: Which Is Cheaper When You Need Money Fast?

- SIP vs Lump Sum: Which Strategy Actually Makes More Money

Disclaimer: All cost figures in this article are estimates based on publicly available 2026 data and are for general educational purposes only. Actual car ownership costs will vary significantly by city, vehicle model, driving habits, fuel prices, and individual circumstances. Returns on investments mentioned are illustrative and not guaranteed — past performance is not indicative of future results. Depreciation figures are based on IRDAI’s standard insurance schedule and may differ from actual market resale values. This article does not constitute financial or investment advice. Please consult a SEBI-registered financial advisor or Chartered Accountant before making significant financial decisions. Data accurate as of June 2026.

Sources: Petrol prices in India today — Goodreturns (June 26, 2026) * Car loan interest rates May 2026 — Zee Biz (May 2026) * Car loan interest rates 2026 — BankBazaar (June 2026) * Car depreciation rate in India — Coverfox (March 2026, IRDAI depreciation schedule) * Total cost of owning a car in India 2026 — AutoIndiaDaily (April 2026) * RTO charges for new cars in India 2026 — PB Partners (2026) * IRDAI official website — motor insurance depreciation schedule

He figured out most of what he knows about personal finance not from courses or advisors, but from years of reading, making mistakes, and fixing them. The Salary Investor is his attempt to save other salaried Indians the same time and money.

He is not a CA or a SEBI-registered advisor. He writes as a fellow salaried person who has been in the trenches — navigating EPF, ITR, 80C, salary slips, and market volatility.

- RSU Taxation India: The Two-Stage Tax Bill That Surprises Every Tech Employee - July 8, 2026

- Credit Card India: How to Earn ₹15,000+ in Rewards, Avoid the Traps, and Never Pay Interest (2026 Guide) - July 6, 2026

- Buy a Home or Keep Renting? The Framework Every Salaried Indian Needs in 2026 - July 5, 2026