Form 121 Explained: The New Form That Replaced 15G and 15H from April 2026

The bank teller looked at Suresh’s 15G form and shook her head.

“Sir, yeh form nahi chalega ab. Naya form chahiye.”

Suresh, 58, took early retirement last year. His only income is ₹2.1 lakh annually from a fixed deposit — well below the taxable limit. He had been filing Form 15G with the same branch for eleven years. The bank had never called to tell him anything changed. His relationship manager hadn’t sent a WhatsApp. He only found out when the TDS was already deducted.

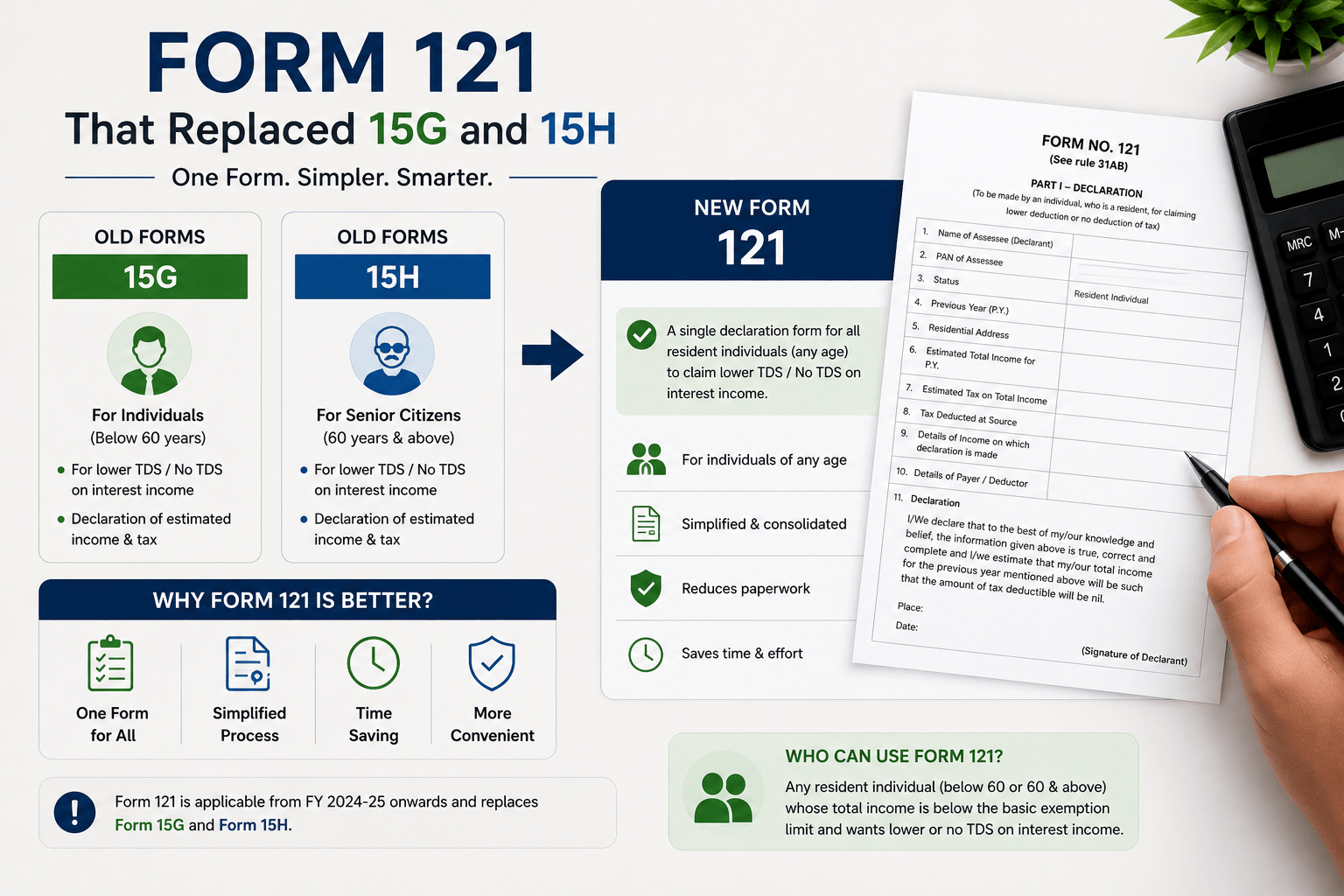

This played out across thousands of bank counters in April 2026. The Income Tax Department replaced both Form 15G and Form 15H with a single unified declaration — Form 121 — effective April 1, 2026, under the new Income Tax Act, 2025. If you submitted 15G or 15H for FY 2025–26, those forms have expired. They do not carry forward. Not even partially.

This article tells you exactly what Form 121 is, who qualifies, which income it covers, and how to actually submit it — including one specific eligibility condition that is tripping up senior citizens who got used to the old Form 15H rules.

What This Article Covers

Why the Old System Was Two Forms in the First Place

The original logic was straightforward: older people needed a different form because they had a higher basic exemption limit. Form 15G was for anyone below 60. Form 15H was for senior citizens aged 60 and above. Same purpose, different paperwork.

In practice, this created constant friction. Someone who turned 60 in November would wonder: which form do I submit in April? A 59-year-old submitting 15H would get the form rejected. Someone submitting 15G when they should have used 15H — or vice versa — lost the TDS exemption entirely and had to wait for a refund by filing their Income Tax Return (ITR).

Both forms also used old legal terminology — ‘Assessment Year’, ‘Name of Assessee’, mandatory section code references — that confused anyone who wasn’t familiar with tax jargon. They required ITR filing history for the last six years. They accepted either PAN (Permanent Account Number) or Aadhaar as identification.

The Income Tax Act, 2025, effective April 1, 2026, simplified the entire framework. Forms 15G and 15H were merged into a single Form 121 under Section 393(6) of the new Act, read with Rule 211 of the Income Tax Rules, 2026.

One form. For everyone. Regardless of age.

What Form 121 Is — and What It Actually Does

Form 121 is a self-declaration form. You submit it to the institution that pays you income — your bank, post office, employer (for EPF-related matters), insurance company, or mutual fund house — to declare that your estimated total income for Tax Year 2026–27 will result in zero tax liability.

Once you submit it, that institution stops deducting TDS (Tax Deducted at Source) from the specific income you declared. That’s the whole point.

What it doesn’t do: Form 121 does not reduce your income, create a deduction, or change your tax slab. It simply prevents TDS from being deducted when you have no tax liability to begin with.

The legal basis: Section 393(6) of the Income Tax Act, 2025, confirmed by the Income Tax Department on its official portal at incometax.gov.in.

And one terminology note worth knowing: Form 121 uses the phrase ‘Tax Year’ instead of ‘Financial Year’. Under the Income Tax Act, 2025, the financial year beginning April 1 and ending March 31 is now called the Tax Year. Tax Year 2026–27 means April 1, 2026 to March 31, 2027 — same period, different label.

Who Can File Form 121 — and the Eligibility Condition Most People Miss

You can file Form 121 if:

- You are a resident Indian (NRIs are not eligible — no exceptions)

- You are an individual (any age) or a Hindu Undivided Family (HUF)

- Your estimated total income for Tax Year 2026–27 — from every source combined — is below the applicable basic exemption limit

- Your estimated tax liability for the year is nil

| Tax Regime / Category | Basic Exemption Limit (Tax Year 2026–27) |

| New tax regime (all ages) | ₹4,00,000 |

| Old tax regime — below 60 years | ₹2,50,000 |

| Old tax regime — senior citizens (60–79 years) | ₹3,00,000 |

| Old tax regime — super senior citizens (80+ years) | ₹5,00,000 |

You cannot file Form 121 if:

- You are a company or a partnership firm

- You are an NRI

- Your total income exceeds the applicable exemption limit above — even if your final tax after Section 87A rebate is zero

That last condition is the one catching people off guard. Here’s a real example.

Meera is 45. She has salary income of ₹5.2 lakh and FD interest of ₹60,000. Total income: ₹5.8 lakh. Under the new tax regime, her tax computes to ₹28,000. Her Section 87A rebate covers ₹25,000. Final tax payable: ₹3,000. She cannot file Form 121, because her total income exceeds ₹4 lakh — the basic exemption limit.

Now compare with Prakash, 67, retired. His only income is ₹2.6 lakh from post office FDs. Under the old tax regime, his basic exemption limit is ₹3 lakh. His income is below that. Final tax: nil. He can file Form 121.

The key change for senior citizens specifically: under the old Form 15H, a senior citizen could file even if their income exceeded the basic exemption limit, as long as the final tax after deductions was nil. That flexibility is gone under Form 121. The rule is now uniform for everyone: income must be below the basic exemption limit.

One more specific restriction for HUFs: an HUF can use Form 121 to prevent TDS on interest income, but not on dividend income. This restriction was in the old Form 15G and continues under Form 121.

Which Income Types Does Form 121 Cover?

As confirmed by EPFO’s (Employees’ Provident Fund Organisation) web circular dated April 13, 2026 and the Income Tax Department’s official FAQ, Form 121 can be submitted to prevent TDS on the following:

- Bank FD (fixed deposit) and RD (recurring deposit) interest

- Savings account interest above ₹10,000

- Post office FD, SCSS (Senior Citizens’ Savings Scheme), and NSC (National Savings Certificate) interest

- Dividends from shares and mutual funds

- Rental income

- Insurance commission

- Life insurance policy payouts

- Income from mutual fund units

- EPF (Employees’ Provident Fund) withdrawals — specifically where TDS would otherwise apply (early withdrawal before completing five years of continuous service)

- Debenture and bond interest

The EPF point is worth flagging separately, because many salaried employees don’t know it. If you resign from a job before completing five years of continuous service and withdraw your EPF balance above the prescribed threshold, TDS applies. If your total income for that year will be nil, you can submit Form 121 to EPFO at the time of withdrawal to avoid that deduction.

What Form 121 does not cover: salary income. Your employer handles salary TDS separately, based on your salary slip and projected income for the year. That process is unrelated to Form 121.

When TDS Gets Triggered on FD Interest (Before You Submit Form 121)

Banks deduct TDS on FD interest only when the annual interest crosses these thresholds (Source: Income Tax Act, 2025, Section 393):

| Category | TDS Threshold on FD Interest (Annual) |

| Individuals below 60 years | ₹50,000 |

| Senior citizens (60 years and above) | ₹1,00,000 |

If your FD interest stays below these limits, TDS is not deducted in the first place. Form 121 becomes relevant when your interest crosses the threshold — but your total income is still below the taxable limit.

How to Fill Form 121 — Part A (You) and Part B (Your Bank)

Form 121 has two sections:

Part A — What You Fill

- Name, PAN (Permanent Account Number — mandatory, no Aadhaar substitution), address, date of birth, residential status, contact details

- Nature of income being declared (FD interest, dividend, rental, etc.)

- Estimated income from this specific source for the tax year

- Aggregate income declared across all your Form 121 filings this year

- Your estimated total income from all sources for Tax Year 2026–27

- Whether you have already filed Form 121 with any other payer this year (you declare the count)

- ITR filing details for the last two tax years — whether you filed, and income declared

Note the last point: Form 15G used to ask for six years of ITR history. Form 121 only asks for the last two. Simpler, less paperwork.

PAN is non-negotiable. If you submit Form 121 without a valid, active PAN linked to Aadhaar, the declaration is treated as invalid. The bank will deduct TDS at 20% instead of the standard 10% — and you’ll need to claim it back through your ITR. Ensure your PAN is active before you visit the bank.

Part B — What Your Bank or Institution Fills

- Their name, TAN (Tax Deduction and Collection Account Number), PAN, address, contact details

- Your name, PAN, estimated income, and the date they received your declaration

- A UIN (Unique Identification Number) assigned to your specific Form 121 submission

The UIN is entirely new to this system. Every Form 121 submission gets its own UIN — a standardised number that links your declaration to your PAN, the payer’s TAN, and the tax year. The institution then quotes this UIN in its quarterly TDS statement (Form 140), even though no tax was deducted. This creates a traceable audit trail. The Income Tax Department can now verify, at a record level, that TDS was legitimately waived — not just omitted.

What this means for you practically: it’s harder to get away with a false declaration than it was under the old system. The UIN, the monthly upload to the IT e-filing portal, and cross-referencing with your Annual Information Statement (AIS) all work together.

Form 15G / 15H vs Form 121 — What Exactly Changed

| Feature | Form 15G / 15H (old) | Form 121 (from April 2026) |

| Who files it | Two separate forms — split by age | One form for everyone |

| Year basis | Assessment Year | Tax Year |

| Age field | Date of birth required | Simple yes/no if aged 60 or above |

| Identification accepted | PAN or Aadhaar | PAN only — mandatory |

| ITR history required | Last 6 years | Last 2 years only |

| Section code references | Required | Not required |

| Investment account number | Required | Not required |

| Tracking system | No centralised UIN | UIN assigned to every submission |

| Senior citizen relaxation | Form 15H allowed income above the limit if final tax was nil | Not available — uniform rule for all ages |

When to Submit — and What Happens if You Don’t

You must submit Form 121 before the income is credited or before TDS is deducted.

If TDS has already been deducted, Form 121 cannot reverse it. The only path back is filing your ITR and claiming the TDS deducted as a credit. The Income Tax Department then refunds the excess after processing — which typically takes several months and is subject to processing timelines that vary by case.

Submit Form 121 at the start of the tax year — ideally in April. Even if nothing has changed from last year: you must submit fresh, every year, to every payer separately. If you have FDs at SBI, HDFC Bank, and the post office, you submit three separate declarations. One submission does not cover multiple institutions.

Online or offline? Many banks — SBI, HDFC Bank, ICICI Bank, Axis Bank — now allow Form 121 submission through their net banking portals or mobile apps. Cooperative banks and post offices may still accept physical forms. Check with your specific institution before making the trip.

Filing a False Form 121 — What the Law Says

This is worth saying clearly: filing Form 121 when your income exceeds the basic exemption limit is a false declaration. It is not a paperwork error. It is an offence.

Under Section 277 of the Income Tax Act, 1961 (which continues to govern prosecution for prior periods) and the corresponding provisions under the Income Tax Act, 2025, a false declaration under Section 393(6) can lead to rigorous imprisonment of six months to two years, along with prosecution.

The UIN system makes this harder to hide than before. Every Form 121 submitted is uploaded to the Income Tax e-filing portal monthly by the payer. That data sits alongside your AIS (Annual Information Statement), which captures interest income reported by banks. A mismatch between your declared income and what the bank reported to the department is flagged automatically. This wasn’t as systematic under the old forms.

If you are close to the exemption limit and uncertain whether you qualify, consult a CA (Chartered Accountant) before submitting. The risk is not worth it.

What to Do Right Now

- Add up all expected income for Tax Year 2026–27 — FD interest, rent, dividends, EPF payout, anything. If the total is below the applicable basic exemption limit and your tax liability is nil, you qualify for Form 121.

- Confirm your PAN is active and Aadhaar-linked. An inactive or unlinked PAN makes your declaration void. Banks will deduct TDS at 20%.

- Download Form 121 from the Income Tax Department’s official portal at incometax.gov.in under the Downloads section.

- Submit to every payer separately. One FD at SBI and one at HDFC Bank means two separate Form 121 submissions.

- Submit before your first income is credited. Once TDS is deducted, Form 121 cannot recover it.

- Do not use old Form 15G or 15H forms. Banks have been instructed to reject them for Tax Year 2026–27. They are invalid.

- Repeat every year. Form 121 is valid for one tax year only. Resubmit every April.

If you are invested in NPS (National Pension System) or PPF (Public Provident Fund), check whether any withdrawals planned for this tax year will affect your total income eligibility for Form 121 before you submit.

If you are uncertain about which tax regime applies to you and how it changes your exemption limit, the old vs new tax regime comparison on The Salary Investor walks through the numbers.

Related Reading on The Salary Investor

- Old vs New Tax Regime: Which One Is Actually Better for You in 2025–26?

- EPF Mistakes Salaried Employees Make — and How to Avoid Them

- How to File Your ITR Yourself — Complete Guide for Salaried Indians

- How to Transfer Your EPF When You Change Jobs — The Complete 2026 Guide

- NPS Exit Rules Explained: How to Withdraw from NPS at Retirement and Before

Disclaimer: The information in this article is current as of June 2026 and is based on the Income Tax Act, 2025, and Income Tax Rules, 2026. Tax laws are subject to amendment. Tax outcomes depend on individual income, applicable deductions, and the tax regime chosen. This article is intended for general financial education only and does not constitute tax, legal, or investment advice. Please consult a SEBI-registered financial advisor or a qualified Chartered Accountant before acting on any information provided here.

Sources: Income Tax Department — Income Tax Forms and Form 121 FAQ (incometax.gov.in, 2026) · Form No. 121 (Earlier Form Nos. 15G & 15H) · ClearTax — Form 121: How to Fill and Submit, Replaces Form 15G and 15H (Tax Year 2026–27) · EPFO Web Circular on Form 121 for EPF Withdrawals — April 13, 2026 (epfindia.gov.in) · CAclubindia — Form 121: New Single TDS Declaration for All Eligible Taxpayers 2026 (April 25, 2026) · BusinessToday — Income Tax Rules 2026: Form 121 Simplifies TDS Process for Senior Citizens (April 1, 2026) · TaxAdda — TDS Rate Chart and Section 194A Threshold Limits FY 2025–26 and 2026–27

He figured out most of what he knows about personal finance not from courses or advisors, but from years of reading, making mistakes, and fixing them. The Salary Investor is his attempt to save other salaried Indians the same time and money.

He is not a CA or a SEBI-registered advisor. He writes as a fellow salaried person who has been in the trenches — navigating EPF, ITR, 80C, salary slips, and market volatility.

- RSU Taxation India: The Two-Stage Tax Bill That Surprises Every Tech Employee - July 8, 2026

- Credit Card India: How to Earn ₹15,000+ in Rewards, Avoid the Traps, and Never Pay Interest (2026 Guide) - July 6, 2026

- Buy a Home or Keep Renting? The Framework Every Salaried Indian Needs in 2026 - July 5, 2026