The Hidden Costs of Owning a Car That Nobody Talks About

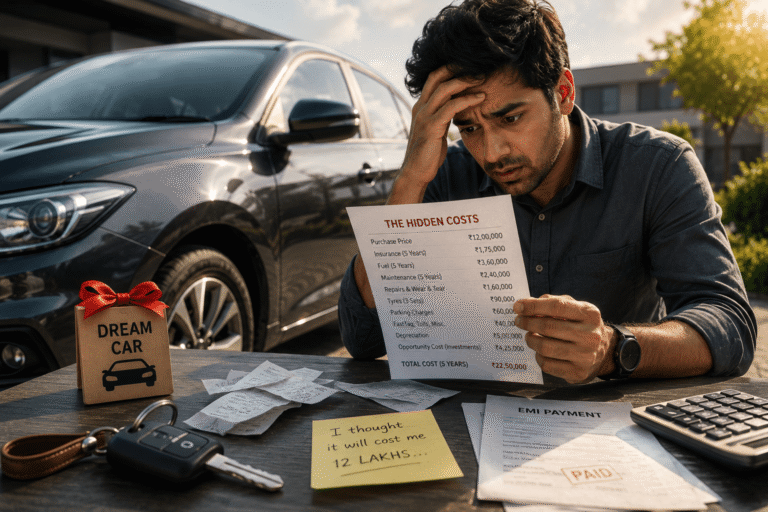

Your ₹10 lakh car may actually cost ₹18 lakh over 5 years — and your dealer never showed you this math. Here’s the full breakdown nobody talks about.

Your ₹10 lakh car may actually cost ₹18 lakh over 5 years — and your dealer never showed you this math. Here’s the full breakdown nobody talks about.

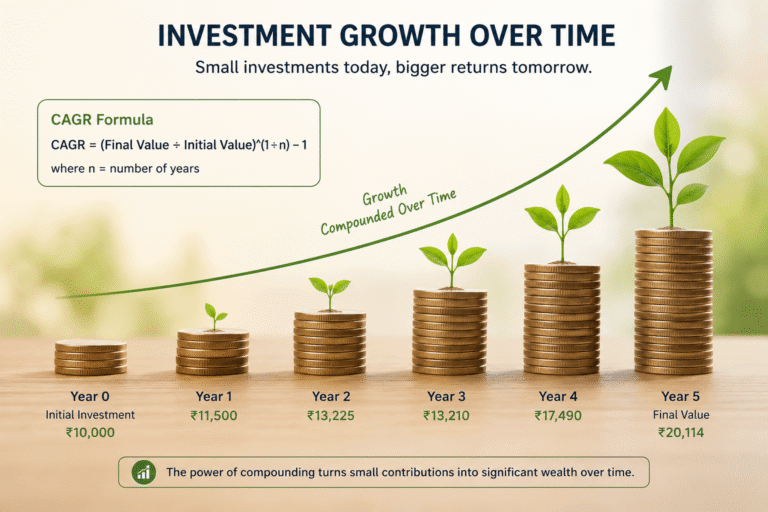

Your mutual fund says 40% returns. But is that real? CAGR vs XIRR vs absolute return — most investors use all three wrong. Here’s exactly which one to use, with real ₹ examples and a step-by-step XIRR calculator guide.

Form 16 late, or the numbers don’t add up? Here’s exactly what the law says your employer owes you — and how to file by July 31 either way.

One mutual fund redemption can force you out of ITR-1. Here’s the 2026 rule that decides whether you stay simple or switch forms.

Your client deducted TDS and you didn’t even notice. Here’s the ITR form, the tax math, and the law everyone’s getting wrong this filing season.

Your employer just replaced Form 12BB with Form 124 — and if you don’t submit it, they’ll deduct TDS as if you have zero savings. Here’s exactly what changed and what to do now.

Your salary didn’t change. Your take-home did. The new wage code 2026 forces basic salary to 50% of CTC — and it quietly changes your PF, gratuity, and tax in ways your HR won’t explain upfront.

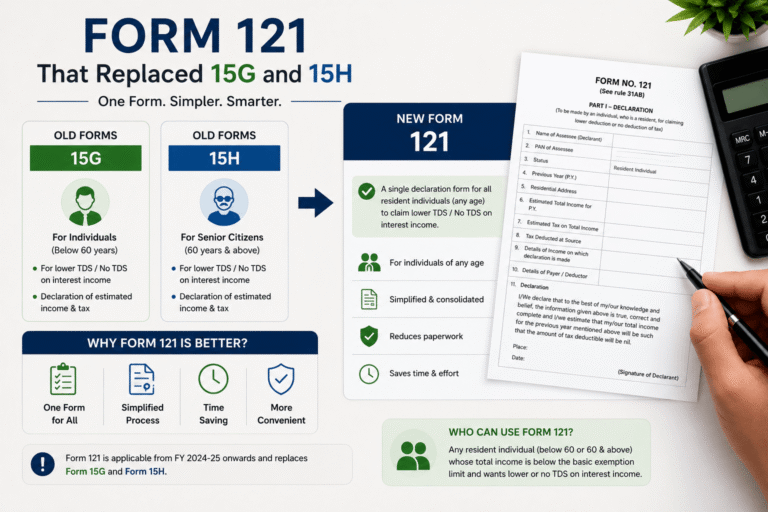

Form 15G and 15H are dead from April 2026. If you submit them, TDS will still be deducted. Here’s exactly what Form 121 is, who qualifies, and what to do before your bank cuts the tax.

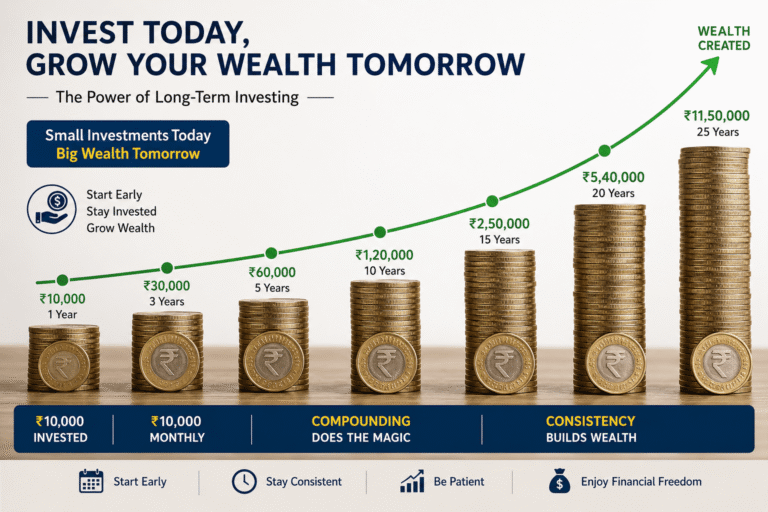

Most investment advice is quietly written for people earning ₹10 lakh+. This one isn’t. Here’s exactly how to start investing on ₹5 lakh or under — with real numbers and no filler.

Health insurance for a 65-year-old costs ₹70,000 a year — before medicines, physio, and caregiver bills. Here’s the insurance, tax, and corpus plan you actually need.

Personal Finance · For Salaried Indians

SIPs, ITR filing, 80C, EPF, insurance, home loans — explained by someone who gets a salary too. No jargon. No course to sell. Just clear answers to the questions you're already Googling.